No doubt, the image of the present market is a fancy mixture of positives and negatives, partly relying on the time interval in query and what’s being checked out.

The economic system has carried out higher than many had predicted, and client confidence has been rising – in all probability to be additional boosted in Could with a Coronation bounce. On the eleventh Could the MPC put up rates of interest for the twelfth time, elevating the financial institution base charge to 4.5%. This can carry additional strain to these on variable charge mortgages as properly these coming off their present fastened charge. It’ll affect these getting into the housing marketplace for the primary time, alongside the two million households resulting from remortgage their fastened charge loans this yr, and for whom a pointy charge rise might be felt as a consequence of the speed rises in 2022 and 2023. Given that each one these could have cleared earlier stress check hurdles, most will cope – however it’s nonetheless loads to soak up.

As this means, affordability might be a key driver, and households have been searching for to deal with the rising pressures ensuing from rate of interest and home value rises by taking out long run mortgages, with some two thirds of mortgages now on the “most” time period of 40 years – up from 50% 4 years in the past.

The expectation is that not solely are we close to the height within the rate of interest cycle, however that the mortgage market has stabilised, and market competitors will give some assist to would-be debtors. The variety of mortgage merchandise has elevated, and we now have 100% loans accessible which recognise a renter’s fee file. Certainly, there have even been recommendations that the federal government may revive the Assist to Purchase scheme, reflecting the essential place housing points have within the political panorama.

Mortgage approvals had been up in March at 52,000, and on the highest stage since October 22. This was above expectations, and though the RICS’ housing market survey outcomes for April had been somewhat combined, the 12-month outlook had strengthened. This implies that though the e.surv Acadata survey highlights persevering with declines within the charge of value progress, home costs themselves must a level stabilised at an England and Wales stage (although in fact with vital regional and native variations). As soon as the market has absorbed any rate of interest rises, patrons are more likely to take a constructive view of the medium-term outlook and be much less anxious about any short-term fluctuations. Spring has arrived, and a level of elevated optimism is turning into obvious.

Richard Sexton, Director at e.surv, feedback:

“Whereas many commentators have focussed on the discount and in some cases falls in home value progress, it’s necessary to place these into context. For the reason that pandemic in March 2020, now we have seen home costs rise by £60,000 or 20% and the next discount of just below £5000 from the height in October 2022 is an effective place from which to do that.

“Now greater than ever, we must always remind ourselves that month-to-month tendencies, usually sparked by non-housing financial tendencies, don’t change some fundamentals concerning the market.

“The continued lack of provide and present affordability points are stymying exercise but additionally assist costs partly as a result of there merely isn’t sufficient of the proper of housing available in the market. The extent to which that is the case has been the acknowledgement by each most important political events this month that housing might be a key election problem. We have now heard already concerning the mooted return of Assist-to-Purchase and different market led mortgage merchandise to assist new patrons.

“We’re solely simply previous April – a key month for patrons and sellers and it’s too early to say whether or not this key month within the housing calendar will herald a return to extra regular progress trajectory. However regardless of the subsequent couple of months carry, our information suggests undue ranges of pessimism are in all probability misplaced.”

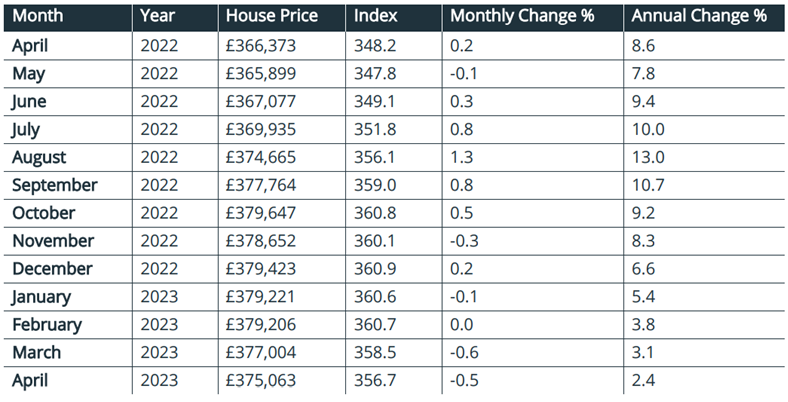

Desk 1. Common Home Costs in England and Wales for the interval April 2022 – April 2023

Notice: The e.surv Acadata Home Value Index gives the “common of all costs paid for home properties”, together with these purchases made with money.

Notice: The e.surv Acadata Home Value Index gives the “common of all costs paid for home properties”, together with these purchases made with money.

Commentary: John Tindale and Peter Williams, Acadata Senior Analysts

Determine 1. The typical home value progress in England and Wales, April 2021 – April 2023

On an annual foundation, the typical sale value of accomplished residence transactions in England and Wales in April 2023 rose by some £8,700, or 2.4%. That is the bottom charge of annual enhance since June 2020, and is the eighth month in succession wherein the annual charge has fallen. On a month-to-month foundation, the typical value fell in April 2023 by round £1,940, or -0.5%. April is a key month within the transactions calendar, with patrons in addition to sellers lively available in the market. Right here we see that, regardless of this, each annual and month-to-month charges present proof of constant reductions in value progress.

On an annual foundation, the typical sale value of accomplished residence transactions in England and Wales in April 2023 rose by some £8,700, or 2.4%. That is the bottom charge of annual enhance since June 2020, and is the eighth month in succession wherein the annual charge has fallen. On a month-to-month foundation, the typical value fell in April 2023 by round £1,940, or -0.5%. April is a key month within the transactions calendar, with patrons in addition to sellers lively available in the market. Right here we see that, regardless of this, each annual and month-to-month charges present proof of constant reductions in value progress.

Nonetheless, as Determine 1 illustrates by way of precise nominal costs, the autumn in value in April 2023 is comparatively minor, particularly when in comparison with the cumulative £43,360 rise in costs since August 2021. In reality, costs have risen by some £60,000, or 19%, for the reason that begin of the pandemic in March 2020, in comparison with a fall of some £4,600 from the height value achieved in October 2022, at £379,647 – so some perspective is required in figuring out the extent of the present value falls.

Common Annual Regional Home Costs

Determine 2. The annual change within the common home value for the three months from February to April 2023, analysed by GOR

Determine 2 exhibits the proportion change in annual home costs on a regional foundation in England and for Wales, averaged over the three-month interval of February to April 2023, in comparison with the identical three months in 2022. These figures are produced on a rolling three-month foundation to easy out minor adjustments in value which can come up, and are centred on March 2023 (pink line), with Determine 2 additionally exhibiting the similarly-averaged figures for February 2023, one month earlier (blue line). The Acadata costs are additionally adjusted for seasonal variation.

Determine 2 exhibits the proportion change in annual home costs on a regional foundation in England and for Wales, averaged over the three-month interval of February to April 2023, in comparison with the identical three months in 2022. These figures are produced on a rolling three-month foundation to easy out minor adjustments in value which can come up, and are centred on March 2023 (pink line), with Determine 2 additionally exhibiting the similarly-averaged figures for February 2023, one month earlier (blue line). The Acadata costs are additionally adjusted for seasonal variation.

As will be seen, the adjustments in common home costs during the last twelve months stay constructive in 9 of the ten GOR areas, with Larger London being the one space the place costs have fallen over the interval. Nonetheless, all ten areas now have a charge of progress of 6.0% or much less – simply three months earlier, in December 2022, the very best regional charge was almost double this at 11.0%.

Since final month, the speed of progress of home costs has fallen in eight of the ten areas, with solely the North East and Larger London seeing larger progress this month (March) in comparison with final. The biggest fall was within the West Midlands, down by 1.8% from 7.8% to six.0%, adopted by the North West, down 1.3% from 4.1% to 2.8%.

Regardless of having the largest fall in costs, the West Midlands stays the highest area for the third month operating by way of the speed of value progress, at 6.0%. This month Herefordshire, Warwickshire and the West Midlands unitary authority (which incorporates Birmingham) have been the area’s high performers, with annual value progress of 11.8%, 8.9% and 6.8% respectively.

Wales, with 5.3% progress, is in second place this month, having pushed the South West area into third place. In Wales, there are three native authority areas, all in South Wales, with value progress in extra of 10%, these being the Vale of Glamorgan (19.0%), Newport (11.6%) and Bridgend (10.1%).

As already famous, Larger London is the one GOR space with unfavorable progress, at -1.9%, though this was really 0.2% larger than the -2.1% seen within the earlier month. In March 2023, 17 of the 33 London boroughs noticed costs rise on an annual foundation (4 fewer than the earlier month). Broadly, it continues to be the costliest interior areas which might be recording falling costs – impacting eight of the highest ten boroughs ranked by value. For instance, within the Metropolis of Westminster – which is ranked in second place in London by way of its common worth – home costs have fallen by -33.2% during the last twelve months, whereas in Kensington and Chelsea – the costliest borough in London – costs fell by -17.1%. In the meantime, 12 of the 16 lowest-priced London boroughs have seen their costs rise during the last twelve months, the 4 exceptions being Tower Hamlets (-15.9%), Newham (-3.6%), Enfield (-3.1%) and Bromley (-1.2%). Tower Hamlets has the second-highest proportion of flat gross sales of the 33 boroughs in Larger London, at 93%.

England and Wales Regional Warmth Map

These completely different tendencies are then evident within the Regional Warmth Map proven beneath for March 2023.

There are maybe three teams in England and Wales in March 2023 by way of home value progress. First are 5 areas with value progress of 4.8% or larger, being the East and West Midlands, Wales, Yorkshire and the Humber and the South West. There then comply with 4 areas the place value progress lies between 2.8% and 4.0%, that are the 2 areas surrounding Larger London, the East of England and the South East, to which we will add the North East and the North West. Lastly, there’s Larger London by itself, with costs falling on an annual foundation by -1.9%.

Annual Development Charge

Annual Development Charge

The annual progress charge in England and Wales in April 2023, for each mortgage and cash-based home purchases, was an arithmetic common of two.4%. That is 0.7% beneath the revised charge of three.1% in March 2023, and represents the eighth month in succession wherein the annual charge of home value progress has slowed. It’s nevertheless the smallest discount in these eight months, maybe suggesting a slowing within the charge at which home costs are falling.

In March 2023, 102 of the 110 Unitary Authority areas in England and Wales had been nonetheless recording home value positive factors during the last twelve months, indicating the large extent of value rises that had taken place throughout the 2 international locations, even when the expansion charge is now diminishing. It’s notable that there are solely eight areas with value falls outdoors of Larger London, the place 16 of the 33 boroughs in March had been seeing declining costs over the yr.

The eight areas in England and Wales which didn’t file a value enhance over the yr had been, from North to South, County Durham (-1.7%), Cumbria (-0.1%), Blackpool (-4.0%), Flintshire (-1.1%), Gwynedd (-8.0%), Rutland (-2.7%), Buckinghamshire (-1.6%) and Bracknell Forest (-6.0%). The somewhat alarming fall in costs of -8.0% in Gwynedd is brought on by the acquisition of a £2 million indifferent residence in Abersoch in March 2022 – this sale was not repeated in 2023, and brought on common costs to fall. The typical value of a indifferent property in Gwynedd in 2023 is nearer to £325k.

The realm with the very best annual enhance in costs in March 2023 is the Vale of Glamorgan, at 19.0% progress – the typical value of each indifferent and semi-detached properties within the Vale having elevated by some £100k during the last twelve months, to £575k and £405k respectively. The rise within the common value of indifferent properties within the Vale was assisted within the month by the sale of a £2.6 million five-bedroomed property in Penarth. Penarth is situated some three miles to the south of Cardiff on the Severn Estuary coast – it’s identified regionally as “The Backyard by the Sea” resulting from its massive variety of parks and open areas – which ticks the brand new hybrid necessities of getting each house in addition to a straightforward commute to the workplace. We’d additionally spotlight the divergence throughout Wales, with the market’s efficiency within the Vale contrasting sharply with that in Gwynedd in North Wales.

Month-to-month Change

Common home costs fell by £1,940, or -0.5%, in April 2023 – this fall was solely £260 lower than the autumn in March, however the two months collectively characterize the most important lower since April 2021– the month after the SDLT tax vacation in England and the LTT tax vacation in Wales had been initially resulting from be withdrawn. In reality, the LTT vacation in Wales was prolonged to June 2021, and the SDLT vacation was prolonged to September 2021 in England, though at decrease charges from 1 July 2021 onward.

In March 2023, costs rose on a month-to-month foundation in 37 of the 110 Unitary Authorities, which is 20 fewer than in February, persevering with the development established over the earlier month of a decline within the variety of authorities the place costs are rising. The realm with the best enhance in costs in March was the Isle of Anglesey, up by 5.1% within the month. Indifferent properties on the Island had the very best enhance in within the month, assisted by the acquisition of a three-bedroomed bungalow, with gorgeous views over the Menai Strait, for £600k. The second-placed authority by way of value progress over the month is the Vale of Glamorgan, additionally with a 5.1% value enhance, as described above. In third place is Windsor and Maidenhead, up by 4.7%, the place the acquisition of a £6.4 million five-bedroom indifferent residence, on the riverside in Bray, helped to boost costs. Maidenhead, which is near Bray, has a 20-minute prepare service into Paddington, which provides to the desirability of dwelling within the space.

The North East was the one GOR space in England and Wales which noticed costs enhance throughout March 2023, in comparison with seven GOR areas with value rises in February. Within the North East, the areas with the very best enhance in costs within the month had been Hartlepool (+3.5%), Northumberland (+3.2%) and Darlington (+2.2%). These will increase had been enough to supply the North East area with a brand new file common value, of £202,451.

Comparability of Indices

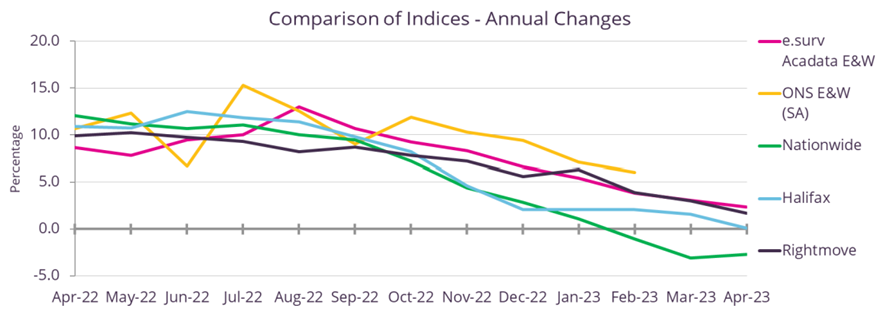

Determine 3. The annual change in home costs April 2022 – April 2023

Determine 3 illustrates the annual charge of change in home costs as measured by the 5 completely different index suppliers listed within the legend to the best of the graph, for the interval April 2022 to April 2023. Normally, the indices agree that the speed of progress has been slowing over time, though there’s a distinction in opinion as to precisely when the upward motion in costs reached its peak, and the pace of its subsequent descent.

Determine 3 illustrates the annual charge of change in home costs as measured by the 5 completely different index suppliers listed within the legend to the best of the graph, for the interval April 2022 to April 2023. Normally, the indices agree that the speed of progress has been slowing over time, though there’s a distinction in opinion as to precisely when the upward motion in costs reached its peak, and the pace of its subsequent descent.

The vary within the charges of progress was at a minimal in September 2022, at simply 2.0%, with e.surv Acadata reporting 10.7%, whereas Rightmove was indicating 8.7%. Following the September figures, it may be seen that, with one or two notable exceptions, the final course of all 5 indices has been downward, however at completely different speeds.

The 2 lender indices – Halifax and Nationwide – had proven remarkably comparable progress charges from September till January, with Nationwide being the primary to announce, in February 2023, that on an annual foundation home costs had turned unfavorable. Halifax got here near following swimsuit this April, exhibiting a constructive annual charge of progress of simply 0.1% over the yr.

The Rightmove and e.surv Acadata’s charges have been converging, with each indices suggesting that costs nonetheless stay larger than twelve months earlier, though the hole between this yr’s and final yr’s costs is narrowing. In the meantime, the ONS index is exhibiting extra volatility than the opposite 4, probably resulting from its coverage of not smoothing (averaging) its outcomes over time. Nonetheless, it too is reporting an identical slope to e.surv/Acadata and Rightmove since October 2022.

There are three most important the explanation why these value indices differ from one another. The primary is to do with the timing of acquiring the value information within the residence buy timeline. Rightmove is the earliest, because it measures its information on the level when a vendor first locations the property available on the market. It’s an asking value, and relying upon the state of the market, negotiations will comply with – up or down reflecting native demand. The 2 lender indices base their information on costs being notified as the applying for a mortgage reaches the mortgage approval stage. Lastly, e.surv Acadata and the ONS each use Land Registry information, which dates the sale on the time of contract completion. That is the ultimate gross sales value.

The second distinction is that the ONS, Rightmove and e.surv Acadata might be recording each money and mortgage-based purchases whereas, by definition, the lenders solely file the costs on their very own loan-based transactions. Lastly, e.surv Acadata and the ONS use all of the home transactions recorded on the Land Registry, whereas the lender indices could properly have insurance policies in place, reminiscent of not lending on properties with a value in extra of £X million, which might introduce a slight bias into their outcomes.

Every has its personal deserves, however it’s helpful to grasp the variations to be able to higher admire what the indices are exhibiting and why they differ. As well as – given the divergence between Halifax and Nationwide this month – the differential make-up of the mortgage portfolio being processed at the moment is mirrored, with the typical value of a Nationwide mortgage being round £30,000 decrease than its rival.

Housing transactions monthly

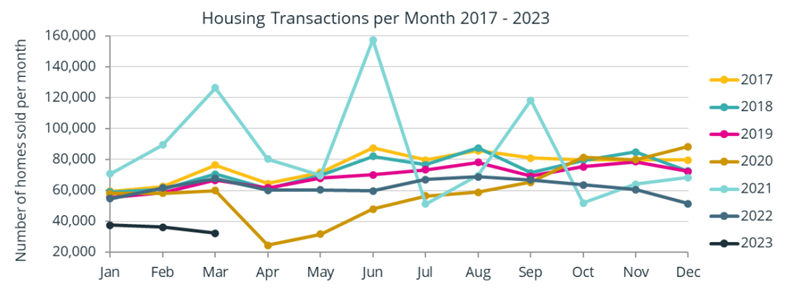

Determine 4. The overall variety of housing transactions monthly, January 2007 – March 2023

Determine 4 exhibits the overall variety of home property transactions monthly recorded on the Land Registry for England and Wales, protecting the interval from January 2017 to March 2023.

Determine 4 exhibits the overall variety of home property transactions monthly recorded on the Land Registry for England and Wales, protecting the interval from January 2017 to March 2023.

There are 4 years of explicit curiosity in Determine 4. The primary is the sunshine brown line of 2020. This yr began with a mean 58,640 transactions within the first three months, as much as the beginning of the pandemic, which was introduced in the course of the later a part of March 2020, when households had been instructed to stay at residence (if not employed in an important service). The announcement got here too late to have an effect on March gross sales, however in April 2020, the variety of property transactions slumped to 24,560. Though property gross sales slowly elevated in the course of the the rest of 2020, the restoration was extended.

Throughout 2021, the sunshine blue line, the housing market was remodeled, partly as a result of tax-holidays that had been made accessible in each England and Wales, and partly owing to the change in angle caused by working from residence coupled with the need for more room. Three spikes are clearly seen in March, June and September 2021, which had been all tax-holiday associated.

Against this 2022, the gray line, proved to be a much more subdued and steady yr than 2021, with transactions returning to a mean 62,000 gross sales monthly – barely forward of the degrees seen in 2020. The discount in gross sales from September 2022 onward is seen, coinciding with each the arrival of Mrs Truss as Prime Minister on 6 September 2022 and the sixth enhance within the official financial institution charge, to 2.25%, on 22 September 2022. Liz Truss departed as Prime Minister on 25 October 2022. The financial institution charge was additional elevated on 3 November and 15 December 2022, ending the yr at 3.5%. Housing gross sales in December 2022 totalled 51,410 – the bottom December complete on the graph.

2023, the black line, has solely seen a mean of 35,000 gross sales monthly – the bottom stage of those three months for the reason that banking disaster of 2009 – however the information for these months remains to be rising, so these totals will slowly enhance over time.

Property varieties

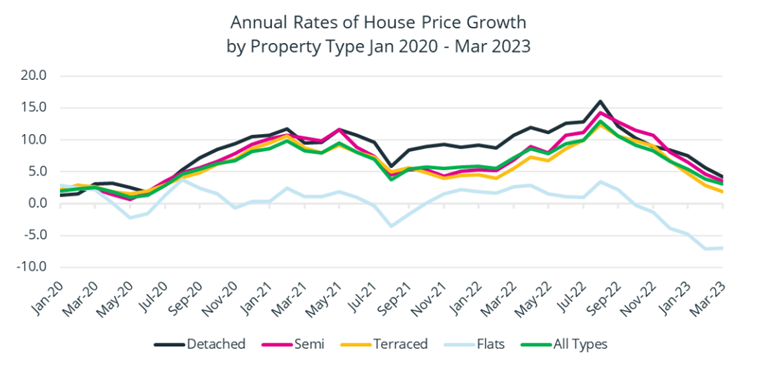

Determine 5. The annual change in home value progress in England and Wales, for the interval from January 2020 to March 2023 by Property Sort

Determine 5 above exhibits the completely different motion in common home costs from earlier than the beginning of the pandemic in March 2020 to March 2023.

Determine 5 above exhibits the completely different motion in common home costs from earlier than the beginning of the pandemic in March 2020 to March 2023.

As will be seen, indifferent properties had the very best charge of value progress over the vast majority of this era, with semi-detached and terraced properties each having decrease charges, broadly comparable to one another. Additionally clear are the far decrease charges of value progress – ceaselessly unfavorable – related to flats over this identical interval.

The excessive charge of value progress for indifferent properties is probably not too stunning. As has been properly documented, the pandemic resulted in life-style adjustments referring to the acquisition of properties, with many patrons searching for out bigger properties to allow them to “do business from home” – which colloquially grew to become referred to as the “Race for Area”. Moreover, different patrons sought out second properties in areas of pure magnificence and coastal areas, to allow them to take “staycations”, or to determine “vacation lets”, as overseas journey grew to become largely prohibited. The resultant competitors for these bigger properties drove up costs.

Flats over this era had been topic to 2 separate elements. Firstly, there was the corollary of the “Race for Area”, in that flats not often have their very own non-public gardens and had been much less more likely to have an additional room which might be transformed into an workplace. Consequently, there was a common tendency for these trying to buy a property to maneuver up the housing chain by way of usable ground space, which diminished the demand for flatted properties. On the identical time, following the cladding disaster related to the aftermath of the Grenfell Tower fireplace, lenders required an EWS1 certificates to make sure the flat was “match for goal”. In lots of instances these certificates proved exhausting to acquire, which equally diminished demand for flatted properties. Therefore the value of flats slipped additional behind different property varieties.

There was latest dialogue that returning to the workplace is now turning into the norm for a lot of staff, no less than on a 3-day per week foundation. This has been accompanied by a motion again to the suburbs of many cities and maybe “pieds-à-terre” in Central and Internal London (not least given the autumn in costs there), to chop down on commuting time and related prices.

Nonetheless, wanting on the value tendencies in Determine 5, there doesn’t look like any clear general winner by way of property varieties, as was the case with indifferent properties in a lot of 2021 and 2022 – though there’s a slight uptick in flats in March 2023 – a development we are going to carefully monitor – though flats are at present dropping worth at a charge of -7.0% every year.

{kind=link}